|

|

Chapter 2 Allocating Economic Resources

I. The Factors of Production

2 Videos

Return to

Economics Internet Library 8/26/23 |

|

|

Chapter 2 Allocating Economic Resources

I. The Factors of Production

2 Videos

Return to

Economics Internet Library 8/26/23 |

|

|||||||||||||||||||||||||||

|

II. The Production Possibility Frontier (Curve)

A. Measures trade off when

producing two types of goods.

C.

Interactive

Model

|

|

||||||||||||||||||||||||||

|

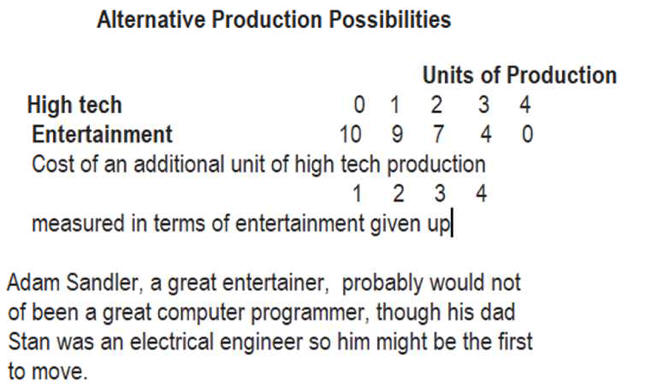

III.

Opportunity Costs

1. The cost of A measured in terms of what must be foregone of B. 2. When considering doing A, we consider the highest valued alternative as limited resources means we can't afford both. 3. For more information visit the Production Possibilities Curve from Wikipedia. 4. Politicians seldom talk of the opportunity cost of what they plan to do. 5. Opportunity Cost Video 5 min 6. Opportunity Cost Lesson/ 7. Covid 19 Opportunity Cost Thought Experiment 8. Examples a. The opportunity cost of good grades is the value which could have been received by spending time with family and friends. b. The opportunity costs of more capital goods is the value which could have been received from having more consumer goods family and friends. c. Opportunity Cost of College explores this example. d. A Lesson in Opportunity Cost e. The Guide to Country Profiles of the CIA World Factbook, 2007 Example 1. U.S. military spending was an about 4.06% of its 2005 GDP. 2. Here is a rank order of country percentages.

3. What are the opportunity costs of high military spendin? 4. CIA, Latest "The World Factbook. Unit III Review The cost of A measured in terms of what must be foregone of B.

|

Our

Free Internet Libraries

|

|

d. Law of Increasing Opportunity Cost video 2min 2.

Quiz

with answers and

What are the opportunity costs of the

Trans-Pacific Partnership?

Unit IV. Review Having additional units of A requires giving up more and more of B. |

Eventually Increasing

3. Readings and Videos a. Production Possibilities Curve Constant and Increasing Opportunity Cost |

| Chapter 2 Class Discussion Questions |

| Chapter 2 Homework Questions |

| Next Chapter |

| Table of Contents |

| Economics Internet Library |