|

|

Overview

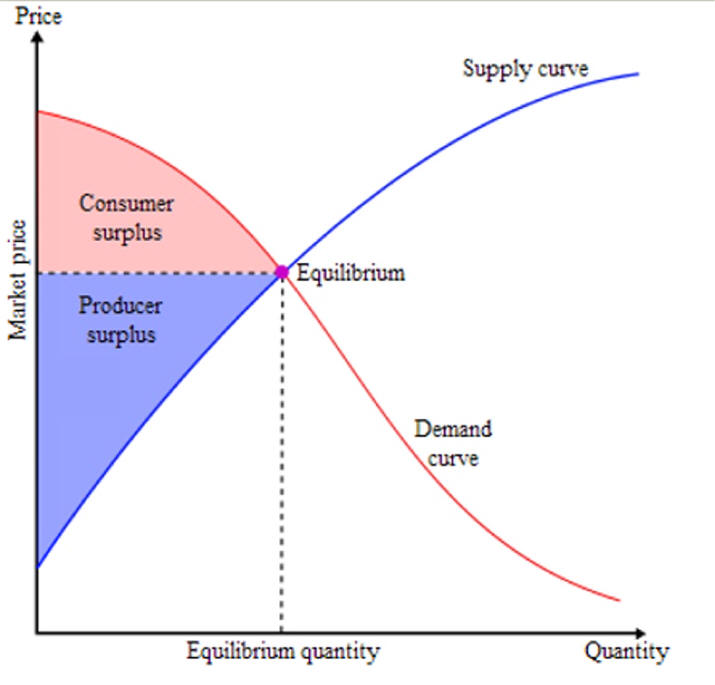

On a standard

supply and demand (S&D) diagram, consumer surplus (CS) is the

triangular area above the price level and below the demand curve,

since intramarginal consumers are paying less for the item than the

maximum that they would pay. In contrary, producer surplus (PS) is

the triangular area below the price level and above the supply

curve, since that is the minimum quantity a producer can produce.

If the

government intervenes by implementing, for example, a

tax or a

subsidy, then the graph of supply and demand becomes more

complicated and will also include

an area that represents

government surplus.

Combined, the consumer surplus, the producer surplus, and the

government surplus (if present) make up the social surplus or

the total surplus. Total surplus is the primary measure used

in

welfare economics to evaluate the efficiency of a proposed

policy.

A basic technique of

bargaining for both parties is to pretend that their surplus is

less than it really is: sellers may argue that the price they ask

hardly leaves them any profit, while customers may play down how

eager they are to have the article.

In

national accounts,

operating surplus is roughly equal to distributed and

undistributed pre-tax

profit income, net of depreciation.

In some schools of

heterodox economics, the economic surplus denotes the total

income which the

ruling class derives from its ownership of scarce

factors of production,

which is either reinvested or spent on

consumption.

In

Marxian economics, the term surplus may also refer to

surplus value,

surplus product and

surplus labor.

Consumer surplus

The individual consumer surplus is the difference between the

maximum total price a consumer would be willing to pay (or

reservation price) for the amount he buys and

the actual total

price.

If someone is willing to pay more than the actual price, their

benefit in a transaction is how much they saved when they didn't pay

that price. For example, a person is willing to pay a tremendous

amount for water since he needs it to survive, however since there

are competing suppliers of water he is able to

purchase it for less

than he is willing to pay. The difference between the two prices is

the consumer surplus.

The maximum price a consumer would be willing to pay for a given

amount is the sum of the maximum price he would be willing to pay

for the first unit, the maximum

additional price he would be willing

to pay for the second unit, etc. Typically these prices are

decreasing; in that case they are given by the individual

demand curve. If these prices are first increasing and then

decreasing there may be a non-zero amount with zero consumer

surplus. The consumer would not buy an amount larger

than zero and

smaller than this amount because the consumer surplus would be

negative. The maximum additional price a consumer would be willing

to pay for each additional unit may also alternating be high and

low, e.g. if he wants an even number of units, such as in the case

of tickets he uses in pairs on dates. The lower values

do not show

up in the demand curve because they correspond to amounts the

consumer does not buy, regardless of the price. For a given price

the consumer buys the amount for which the consumer surplus is

highest.

One

bargaining tactic is to pretend a lower consumer surplus. The aggregate consumers' surplus is the sum of the consumer's

surplus for each individual consumer. This can be represented on the

figure of the aggregate demand curve.

1.

Friedman,

David D

Price Theory: An Intermediate Text - Chapter 9 and

2. Further Reading

Henry George,

Progress and Poverty

[1]

|

|

Calculation from supply and demand

The consumer surplus (individual or aggregated) is the area under

the (individual or aggregated) demand curve and above a horizontal

line at the actual price (in the aggregated case: the equilibrium

price). If the demand curve is a straight line, the consumer surplus

is the area of a triangle:

-

Where Pmkt is the equilibrium price (where supply

equals demand), Qmkt is the total quantity purchased at

the equilibrium price and Pmax is the price at which the quantity purchased would fall to 0 (that is, where the demand curve

intercepts the price axis). For more general demand and supply

functions, these areas are not triangles but can still be found

using

integral calculus. Consumer surplus is thus the definite

integral of the demand function with respect to price, minus the

definite integral of the constant function D(P)=Qmkt

(i.e. PmktQmkt), from the market price to the

maximum reservation price (i.e. the price-intercept of the demand

function):

-

The graph shows, that if we see a rise in the equilibrium price

and a fall in the equilibrium quantity, then consumer surplus falls.

Distribution of benefits when price falls

When supply of a good expands, the price falls (assuming the

demand curve is downward sloping) and consumer surplus increases.

This benefits two groups of people.

Consumers who were already

willing to buy at the initial price benefit from a price reduction;

also they may buy more and receive even more than at the initial price and also receive some consumer

surplus.

Consider an example of linear supply and demand curves. For an

initial supply curve S0, consumer surplus is the triangle

above the line formed by price P0 to the demand line

(bounded on the left by the price axis and on the top by the demand

line). If supply expands from S0 to S1, the

consumers' surplus expands to the triangle above P1 and

below the demand line (still bounded by the price axis). The change

in consumer's surplus is difference in area between the two

triangles,

and that is the consumer welfare associated with

expansion of supply.

Some people were willing to pay the , the by P1,

on the left by the price axis and on the right by line extending

vertically upwards from Q0.

The second set of beneficiaries are consumers who buy more, and

new consumers, those who will pay the new lower price (P1)

but not the higher price (P0).

Their additional

consumption makes up the difference between Q1 and Q0.

Their consumer surplus is the triangle bounded on the left by the

line extending vertically upwards from Q0, on the right

and top by the demand line, and on the bottom by the line extending

horizontally to the right from P1.

Rule of one-half

The rule of one-half estimates the change in surplus for

small changes in supply with a constant demand curve. Note that in

this special case where the consumer

demand curve is linear,

consumer surplus is the area of a triangle. Following the figure

above,

-

where:

- CS = Consumers' Surplus

- Q0 and Q1 are the quantity demanded

before and after a change in supply

- P0 and P1

are the prices before and after a change in supply

|

f

f